The global PET packaging market is worth $48.1 billion in 2014, amounting to almost 16 million tonnes according to a new market report from Smithers Pira. Demand for PET packaging is expected to increase by an average of 4.6% annually over the next five years, and will amount to 19.9 million tonnes worth $60 billion by 2019.

The Future of PET Packaging to 2019 gives an overview of the state of the PET packaging industry in 2014, alongside global market forecasts to 2019, including key definitions and details of specific geographic markets.

According to the report, demand for PET packaging has been on the rise since 2010. PET bottles are becoming more widely used because they are easier to handle, do not break, can be resealed and are light for on-the-go consumption. PET bottles are an increasingly popular type of packaging for carbonated soft drinks, bottled water, ready-to drink tea and functional drinks. PET packaging has also been making inroads into markets for juice, packaged food, household cleaning products and pharmaceuticals, replacing other packaging materials in these end-use sectors.

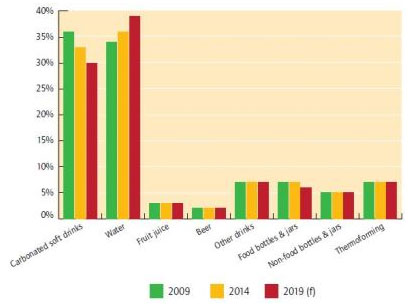

While some packaging producers and brand owners think that there may still be opportunities for further light-weighting of PET bottles over the five years to 2019, others are sure that the limit of lightweighting has been reached. Within overall PET packaging consumption of 15.4 million tonnes in 2013, PET bottles for beverages accounted for over 80% of overall sales at 12.5 million tonnes (up 3.7% on 2012). In 2013, bottled water became the largest category for PET packaging; sales of PET water bottles grew by 7.3% reaching 5.45 million tonnes. Sales of PET bottles for carbonated soft drinks by comparison rose by 1.8% to 5.17 million tonnes. Slower growth of latter is attributed to high penetration rates in major markets and a growing consumer preference for healthier drink options.

According to Smithers Pira, in the key remaining packaging sectors, non-food PET packaging sales reached 804,328 tonnes (a 4.4% increase on 2012 levels), with thermoforming packaging consumption up 4.7% to 1.04 million tonnes. During the period 2014-19, the fastest growing end-use sector will be bottled water bottles with 6% growth in volume terms, followed by pharmaceutical and medical packaging and PET bottles for other drinks, both increasing by 5%.

Figure :Global PET packaging market volume by end-use sector, 2009, 2014 and 2019 forecast (% share)

Source: Smithers Pira

Key market drivers include rising incomes in developing markets of Asia Pacific, South and Central America and Central and Eastern Europe. In terms of geographical regions, Asia Pacific overtook both North America and western Europe during the period 2009-13 to become the largest regional market for PET packaging. The impact of the global recession of 2009 in Asia Pacific was not as severe as in North America and western Europe. Therefore, the growth rates of PET packaging sales have been much higher in this region. In 2014, Asia Pacific commands a 31% share of the global PET packaging market, followed by North America (23%) and western Europe (19%).